The Previously Secret Blueprint To Growing Your Business, Beyond Belief, With Customer Financing

Here’s what you need to understand. Seventy-seven (77%) percent of consumers making a major purchase ALWAYS seek financing and forty-five (45%) of those that made a major purchase say they wouldn’t have done so if not for customer financing.

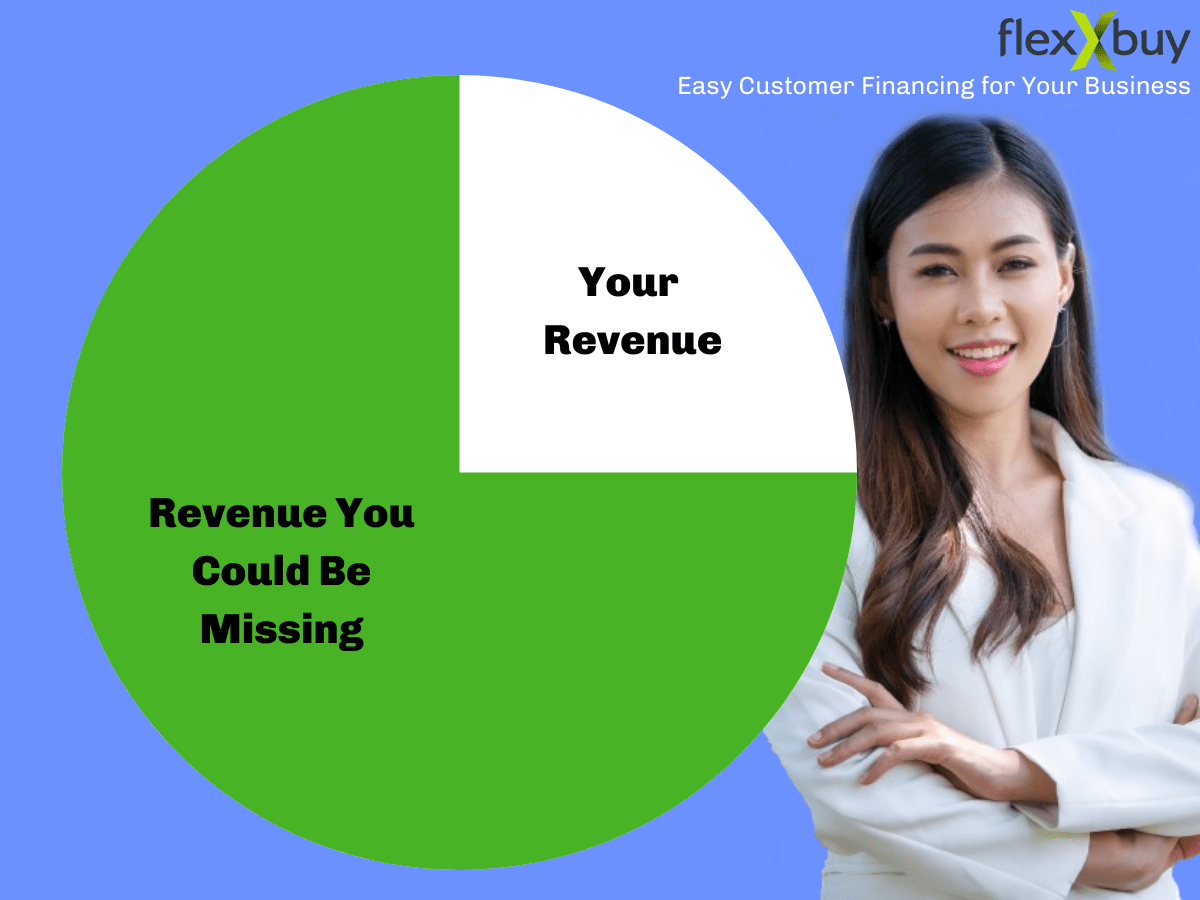

So here’s the question. Is your business operating on all cylinders and in position to capture this very large segment of your customer base?

Don’t kick yourself if you’re not, most businesses are not.

There are a lot of misconceptions when it comes to using customer financing. The most common one is that only desperate people utilize it. The truth is, that consumers across the entire financial and credit spectrum, regardless of demographics and means, seek out financing for their major purchases.

Here’s why. Mentally, we all have our money and credit cards allocated for certain things. When we step into the realm of a purchase that wasn’t in our radar, either due to need or want, we scramble to make the puzzle pieces fit.

Customer financing is powerful because it allows us to allocate a smaller chunk, a monthly payment, into the equation. It’s a lot easier to digest a payment into our monthly budget than it is to depleting our bank account or reducing our available credit.

Customer financing is not just a utility like, let’s say, your credit card processing terminal. It’s been a long time since you likely got a new customer because you accept credit cards. It’s pretty much assumed.

But if you don’t offer customer financing or some kind of buy now, pay later alternative, it’s likely that you are missing out on a chunk of revenue. And while having customer financing is better than not having it, if you don’t utilize it in the way I’m about to show you, money is being left on the table. Actually, the money is not coming close to your table.

Let me start with the three stages of every sale.

It doesn’t matter whether you sell car tires or legal services. Whether you have a coaching business or sell airplanes. The person that ultimately becomes a customer goes through the same flow.

Step 1. Every sale starts with an inspiration. The idea to buy that product or service. The interest and curiosity. But with it, particularly on a major purchase, comes the first thoughts, how much will it cost and how am I going to pay for it? Will I pay for it with my available money or use a credit card? Will I try to finance it? Do I need to finance it? What are my other options?

Step 2. Next comes the engagement. I know what I want and now it’s time to start buying process. Perhaps they will jump on-line and start searching for options or reach into their snail mail bin and search for those weekly circulars. Maybe they’ll make a phone call or get in their car and drive to a store. Now, if if step 1 they determined that they need financing, the list of prospective businesses they will contact will narrow to those that say they offer it. And guess what? When financing is needed, the price of the product or service becomes less important. It now comes down to getting it done at a monthly payment that is affordable.

Step 3. Finally, there’s the close. Coming to terms on the ingredients that make up the final sale. Normally, price is a factor, but if financing is part of the sale, it becomes more about the monthly payment. Think about the last time you bought or leased a car. Do you even know how much you agreed to pay for the car? If you’re like most people, you really only know the monthly payment you agreed to. Would it surprise you that you likely paid more for that car than you would have if you paid cash? It’s not because you were cheated but the paradigm of the sale changed. And it’s likely you purchased more of a car than you came in for.

Sometimes we hear from businesses that their customers don’t need financing. They know this because they don’t ask for it.

It’s really important to understand that forty (40%) percent of consumers live paycheck-to-paycheck and about sixty (60%) percent of consumers don’t have $1,000 in savings should an emergency come up. Do you think that these people are flush with credit cards they can use? And we already know that they are likely to research businesses that offer financing before they make their first move.

If your business is not getting requests for financing, it’s not because they don’t need it, they are going someplace else and becoming someone else’s customer.

(pick up good, better, best narrative)

Bob Lovinger is the President of Flexxbuy, a leading US broker in the area of customer financing. Flexxbuy features a number of multi-lender platforms that can accommodate most business verticals and their customers covering a wide array of credit profiles.

Bob Lovinger is the President of Flexxbuy, a leading US broker in the area of customer financing. Flexxbuy features a number of multi-lender platforms that can accommodate most business verticals and their customers covering a wide array of credit profiles.